-

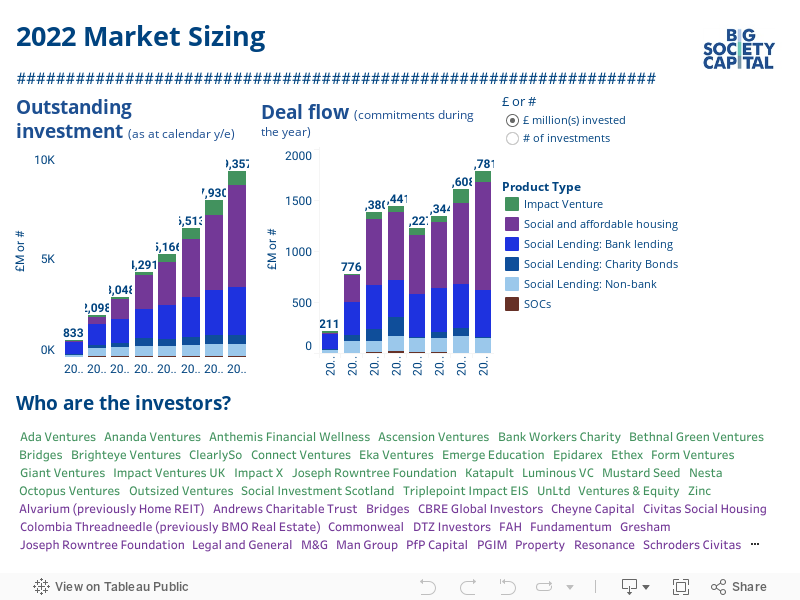

Size of the UK social impact investment market

Our annual market sizing estimates the value of the total market in the UK, and the four areas where we see real opportunity for growth in social impact investment – social property, social lending, impact venture and social outcomes.

- £9.4bn value of social impact investment market at end of 2022, an 18% increase since 2021 – as at 31 December 2022

- 11x eleven-fold growth in eleven years, increasing from £830m in 2011 – as at 31 December 2022

- 6000 the total number of outstanding deals into social impact investment – as at 31 December 2022

Our annual research on the social impact market revealed that in 2022, £1.8 billion was committed across 1,310 investments into projects delivering measurable social impact such as affordable homes, community food banks and tech startups tackling mental health.

Explore the data in the chart and further commentary on the four focus areas below.

-

Social and affordable housing

Social and affordable housing funds account for 55% of the social impact investment market.

How has the market changed?

Outstanding investment in social property funds increased by 35% since 2021 to £5.1 billion at the end of 2022. £1,058 million of deals were committed in 2022, up 35% since 2021.

What caused the changes?

Growth this year was partly thanks to the addition of new funds managed by Legal & General and M&G plc which have met our inclusion criteria for 2022, in addition to new equity raises. The market also saw growth across existing affordable housing funds and funds that support those at risk of homelessness. These include the CBRE Affordable Housing Fund, the Man GPM RI Community Housing Fund, Resonance National Homelessness Property Fund 2 and Social and Sustainable Housing 1.

Where is the investment going?

- Grand Union, which with Man Group has provided 79 new homes to key workers including nurses and bus drivers in Milton Keynes – and the fund overall aiming to deliver 1,295 affordable homes by 2026;

- P3 Charity, which using social investment from managers including Social and Sustainable Capital has provided 300 affordable homes in Gainsborough, Lincolnshire and beyond;

- Notting Hill Genesis with Resonance will manage almost 600 properties aimed at supporting families in the highest need.

-

Social lending

Social lending includes bank, non-bank lending and charity bonds. It is the second largest segment of the market at 37%.

How has the market changed?

Outstanding investment in social lending has increased by 6% since 2021 to £3.5 billion. £616 million of deals were committed in 2022, down 9% since 2021.

What caused the changes?

Social banks – which make up 70% of the social lending market - grew by 7% between 2021-2022, with the value now at £2.5 billion. Leading social banks such as Unity, Charity Bank and CAF Bank continued steady growth trajectories from previous years.

Non-bank lending – which covers all alternative models for lending for impact – was up 4% in 2022, to £605 million. While charity bonds - tradable loans from a group of social investors to a charity or social enterprise – were up 3% in 2022, to £454 million.

There was a sharp increase in deals in 2020-2021 due to the role of alternative lending in channelling emergency capital to where it was needed most during COVID-19. Notably, deals are still higher than the level of 2019, the year before COVID hit.

Where is the investment going?

- New Leaf – a Birmingham social enterprise which helps ex-offenders find employment – which with Sumerian Foundation launched a new ethical recruitment agency.

- Open Kitchen, a sustainable catering business which with Access Growth Fund and Flexible Finance Fund provides affordable meals to Manchester locals.

- Harry Specters, a chocolate company providing employment to young autistic people which using community lending scaled from a kitchen table to factory premises.

Read our new Enterprise Data: Mapping UK social investment survey results – which show the geographical spread of social lending across the UK and which issues it is tackling.

-

Impact venture

Impact venture accounts for 7% of the overall market.

How has the market changed?

Outstanding investment was worth £673 million at the end of 2022. £105 million of deals were committed.

What caused the changes?

We updated our methodology for 2022 to provide a more consistent, accurate picture. If these changes had been in place for 2021, outstanding investment would have grown year-on-year. This is a result of continued investment into the sector and increases in valuations for high-performing impact companies.

The decrease in deals committed since 2021 can be explained by wider market forces; for example, there was a 25% decline in investment across the UK and European venture markets more widely in 2022. [1]

Where is the investment going?

- Switchee – a smart thermostat for social housing which with Ascencion enables social landlords to proactively identify properties at risk of damp or mould and helps users lower their heating bills by up to 17%.

- RideTandem, a mobility app tackling transport poverty which with Ascension and Zinc has completed more than one million passenger journeys.

- Wagestream, a financial wellbeing app which with Ascension Ventures has given over 2 million frontline workers to access fair finance through employers such as Bupa, Next, Co-op and the NHS.

[1] Dealroom data shows UK venture investment fell by 25%

-

Social outcomes contracts

Social outcomes partnerships account for 1% of the overall market.

How has the market changed?

Outstanding investment into social outcomes contracts was £28 million at the end of 2022.

What has caused the changes?

Social outcomes contracts remain a small yet significant part of the market. Big Society Capital’s 2022 analysis shows that in just over a decade the UK has launched 90 projects of this kind. To date this approach has been used by over 180 commissioners, predominantly across local and central Government, involving over 220 social sector delivery partners, and ultimately benefitting over 55,000 people facing complex social challenges.

2022’s market size change since 2021 is a result of methodology changes aimed at ensuring consistency with other parts of the market.

Where is the investment going?

- Middlesbrough charity Open Door which with Bridges Outcomes Partnership and others supports refugees in integrating into the wider community.

- Skill Mill which with Big Issue Invest and others is providing transformational employment and skills to over 200 young ex-offenders across local authorities including Leeds, Birmingham, Durham and Croydon.

- Thrive.NEL social prescribing in Lincolnshire for those with long term conditions including asthma, diabetes and epilepsy, which is reducing NHS secondary care usage by 18.5%.

-

Learn more

Learn moreEnterprise Data 2022: Mapping UK social investment

We explore the geographical spread of social lending across the UK and which social issues it is tackling.

-

Learn more

Learn moreMarket data FAQs

Got a question about the market data? We've put together some frequently asked questions and provided the answers.